Government bonds are subject only to interest rate risk. However, corporate bonds are subject to credit risk in addition to interest rate risk. Credit risk subsumes the risk of default as well asthe risk of an adverse rating change. In this empirical study, we analyze credit rating migration versus yield spread of the bond in US corporate bond market to bring about greater understanding of its credit risk.

DATA

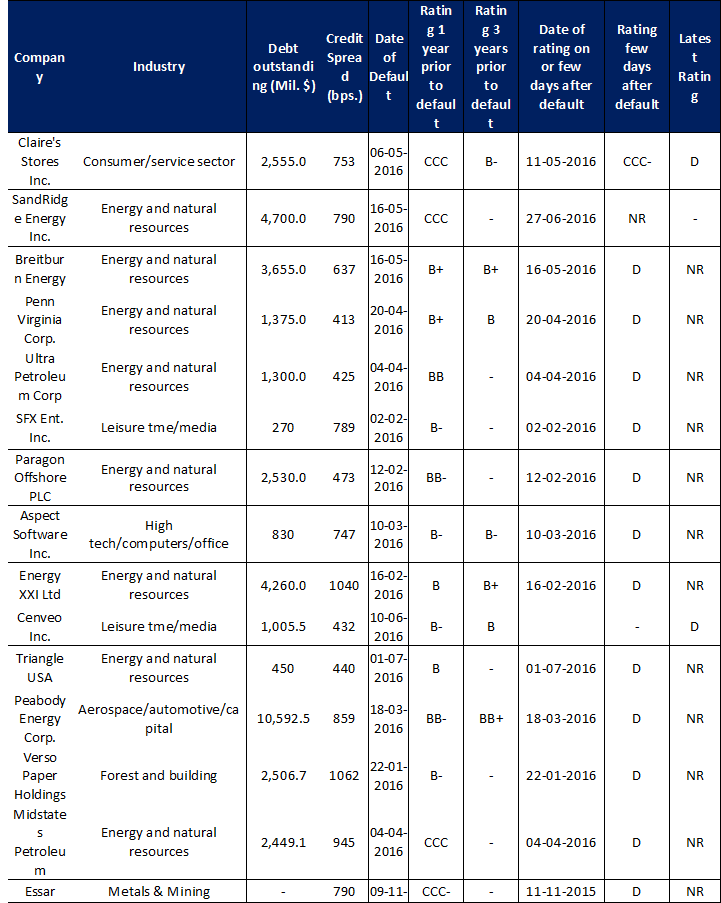

The data for this study consists of ratings of the corporate bonds of US corporate bond market given by S&P Global Ratings and credit spread mentioned under description of the security on the Bloomberg Terminal.The sample consist of 15 corporate bonds issuer companies which have defaulted.

LIMITATION OF THE DATA

Small sample size (Representative Bias)- The sample size for the study is limited to 15 instances of corporate bond default and hence the conclusion cannot be generalized.

METHODOLOGY

One data set focused on the latest available spread of the defaulted US Corporate Bonds. Second data set focused on the before and after credit rating of those defaulted bonds. Both data sets were studied in comparison to figure out which set of data was more predictive of default.

One data set focused on the latest available spread of the defaulted US Corporate Bonds. Second data set focused on the before and after credit rating of those defaulted bonds. Both data sets were studied in comparison to figure out which set of data was more predictive of default.

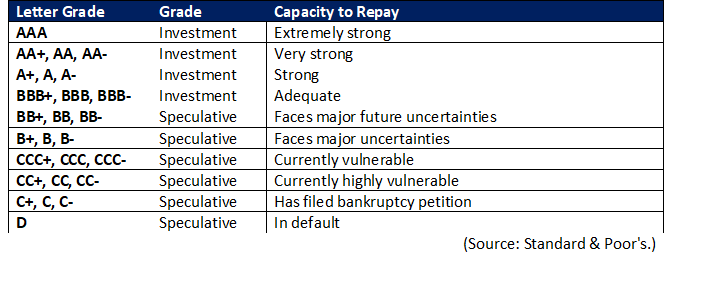

RATINGS AND ITS DESCRIPTION

Following rating grades by Standard & Poor’s are used for analysis:

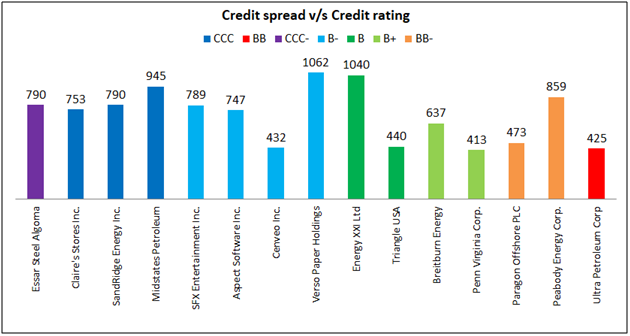

CREDIT RATING v/s CREDIT SPREAD FOR US DEFAULTED CORPORATE BONDS

Following table shows the changes in credit rating and latest credit spread of sampled 15 corporate bonds which defaulted for either of the reasons mentioned as under:

- Missed interest or principal payments: 33% of the sample

- Debt/distressed exchanges: 20% of the sample

- Chapter 11 and Chapter 15 filings–along with foreign bankruptcies—together: 40% of the sample

- Unknown: 7% of the sample

OBSERVATION

The sampled data set reveals that:

- All defaulted corporate bonds have the credit spread of 400 bps or more

- The ratings of 75% of the bonds were changed to D (Default) on the day or within few days after its default

- All the Ratings lie in the ‘Speculative Grade’ defined by S&P Ratings

- Following table summarises the data of credit spread (in bps) and credit ratings of the respective sampled bonds. From blue to red bands, the credit rating decreases. Therefore, red signifies that even though the bond rating was relatively better, the bond defaulted

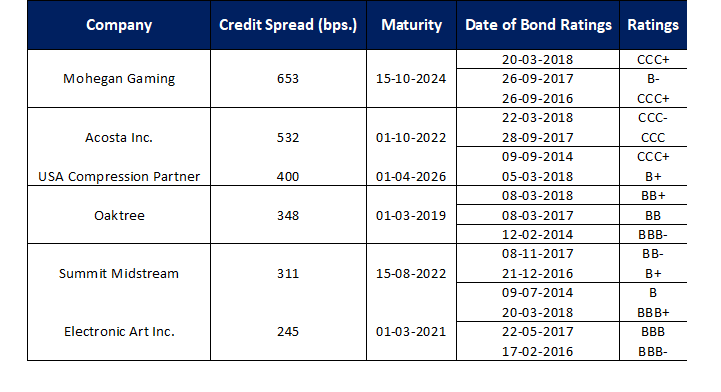

CREDIT RATING v/s CREDIT SPREAD FOR CURRENTLY TRADED U.S. CORPORATE BONDS