Financial advisors have time and again advised investors on creating a Contingency corpus. In fact, one of the basic financial lessons we have learnt from our parents is, always save for a rainy day.

Unprecedented times of global pandemic, lockdown extending to almost 6 months, business shutdown, increasing job loss, have further demonstrated the requirement of having a contingency corpus. A contingency fund provides you with some cushion to fall back on in case of an unexpected income loss.

So how does one start? The first step is to determine the value of your Contingency fund. The average rule is 6 months of fixed expenses in case of single income household or 3 months of fixed expenses in case of multiple income households. Ensure you include your rent, maintenance, grocery and food bill, the education cost in any. In case of an ongoing EMI ensure at least 6 months provisioning even with multiple income households.

Now, once you have estimated the appropriate size of your contingency corpus, how does one go about saving for it and where should you invest the money? The instruments suited for investing the contingency fund is ideally which have high liquidity and focus on capital protection. As it is not the job of a contingency fund to earn a high return. The job of a Contingency fund is to be there in an emergency and should be easily converted into cash.

Contingency fund needs to be divided into multiple components, rather than treating it as one single chunk of money. Instruments like Liquid funds, Ultra short term fund, Fixed Deposits etc. are few of the avenues one could look at investing.

It is also suggested, to keep around 10 to 15 days of your expenses in hard cash at home. Because the emergency can also come in the form of a natural catastrophe, during which banks can remain shut and several ATMs not working.

Rest of the funds can be spread across Deposits and Mutual funds. Do remember as per revised SEBI guidelines, Liquid fund have exit load up to 7 days. Also, while selecting a Liquid fund or an Ultra short term fund ensure the fund has a high quality portfolio. A large portion must be in sovereign or AAA-rated papers and is not mandated towards chasing higher returns.

Do remember to de-risk your contingency corpus, reduce bank risk by spreading out your deposit in more banks and mutual funds also by investing in at least two fund houses.

Since we all know the need for a Contingency fund, why do investors still fail to provide for it or have insufficient funds allocated? One of the major causes is most of the time the investors cannot provide for the entire fund value at one shot and eventually end up not saving enough.

One of the strategy investors should opt for is systematic saving for Contingency Corpus fund too. One can start with a SIP into a liquid fund or ultra-short term fund, many liquid funds have provision for SIP into liquid funds too. Another option is starting a recurring deposit.

Thus, it is never too late to start provisioning for your Contingency fund, you can start small and build up towards the required corpus. Also, now that you are staying at home and are practising social distancing due to COVID-19, you can use this opportunity to save the money you would normally use on things like dining out, travelling to work, vacations etc toward your contingency fund.

As our Grandmother used to say, like an ant save for the rainy day.

Author

Sana Shaikh Volunteer – Wealth Management M. Sc. Finance NMIMS, Mumbai Batch of 2020-22 Connect on LinkedIn

If you have the stomach for stocks but neither the time nor the inclination to do the homework, invest in equity mutual funds

-Peter lynch

When we look at any investment avenue, we mostly consider three aspects–

Historical Returns

Risk / Volatility

Cost

Historical returns

We usually analyze the historic returns in short term (6months to 1-year), medium-term (1-3 years) and long term (>3 years) depending on the investment class and investment horizon. This analysis helps us to form the general expectation of returns over the holding period, disregarding the random walk theory.

Risk / Volatility

Here we compute the standard deviation or movement of returns around the average returns of an investment avenue. Consider two investment avenues, Investment A provides average returns of 15% with standard deviation of 5% and Investment B provides average returns of 20% with standard deviation of 15%

Which amongst the two is riskier?

Answer is investment B- Even though investment B provides higher returns, the potential risk is much higher. A standard deviation of 15% indicates that there is a higher probability of returns lying somewhere in the range of 5% to 35% whereas the returns of investment A can range from 10% to 20% which might be better for a risk-averse investor. The probability of generating returns below 10% is very low in case of investment A.

Apart from the standard deviation, R squared and Beta are also risk indicators that can be used.

Cost

Cost includes tax, transaction cost, brokerage etc.

Taxes on mutual funds can be classified into Stamp duty, Income tax and Security transfer tax

Consider equity- the Stamp duty is 0.015% and 0.003% for deliverable and non-deliverable securities respectively.

Income tax depending on tenor of investment there will either attract Short term Capital gains tax and Long-term capital gains tax.

STT i.e. security transfer tax which is applied on sale of security

Brokerage fees depends on broker person subscribes and services they require.

Costs – And how various costs are affecting your investments over the time. What strategies could use to maximize your returns from mutual funds?

Costs attached to mutual funds are –

Entry load

Exit load

Expense ratio

Taxes

To explain effect of this cost on your portfolio let’s take hypothetical example-

Initial Capital of Rs. 1, 00,000, average annual return of 15%, time horizon of 1, 3, 15, 40

1) Entry Load

It is charge you pay to buy/enter in mutual fund scheme. Which could be up to 2.25%. Entry load is now abolished by SEBI.

Illustration—

Entry Load

2.25%

Investment

100000

Invested

97750

ROI

15%

Value

ROI

1 Year

112413

12.41%

3 Years

148666

14.13%

15 Years

795398

14.83%

40 Years

26183662

14.93%

We can see that effect of entry load on investment in short term and long-term investment horizon. In short run it has more impact than in the long run.

2) Exit Load

Exit load is basically the load for redeeming your units and booking your gains before completing a fixed duration. It is like a penalty charged on exiting, before completing a fixed investment tenor or lock in period. Essentially an exit load in effect is not different from entry load in terms of returns. But unlike the example given above, in practice the exit load is leviable only for a fixed lock in period for which the mutual fund requires the funds. Hence exiting is recommended only after completion especially when the NAV returns are high and expense ratio is low. Usually liquid funds and guilt funds have zero to negligible exit loads given their portfolio and name

3) Expense Ratio:

It is the annual charges levied on the invested capital for financing all expenses.

AUM (Billion Rs)

Equity-oriented

Others (excl. Index funds, ETFs & FOFs)

0 – 5

2.25

2

5 – 7.5

2

1.75

7.5 – 20

1.75

1.5

20 – 50

1.6

1.35

50 – 100

1.5

1.25

100 – 500

Reduction of 0.05% for every increase of 50 billion AUM/ part thereof

Reduction of 0.05% for every increase of 50 billion AUM/ part thereof

>500

1.05

0.8

Total expense ratio of mutual fund scheme Source: SEBI Press release

Regular Plans:

Distribution plays a very important role in last-mile delivery of product and that is true for Mutual funds as an investment product too. It also requires proper distribution for it to reach its target customer. If they are sold through distributors, then there are extra fees levied on investors every year which act as commission for distributor.

Expense heads

% charge

Investment management fees

1.25

Trustee Fees

0.1

Audit Fees

0.01

Custodian Fees

0.01

Registrar & Transfer Agent Fees

0.15

Marketing and Selling Expenses

0.75

Investor communication cost and fund transfer cost

0.15

Other Expenses

0.08

Total Expenses

2.5

Example of breakup of typical mutual fund’s expense ratio of regular plan

Direct Plans:

A direct plan allows investors to invest directly in mutual funds without any intermediary. The benefit of it being that investors don’t pay extra distribution and marketing fees every year.

“SEBI has mandated mutual funds to compulsorily launch a direct plan for direct investments, i.e., investments not routed through a distributor, from 01 January 2013. Such a separate plan has a lower expense ratio excluding distribution expenses, commission, etc., and no commission is to be paid from such plans. The plan also has a separate NAV.”

Illustration – Breakup of any generic Regular Mutual fund

These are expenses that are deducted every year from assets under management. When we look at the above table, we can see that 0.75% is what you pay extra for regular plans every year. Passive funds are usually direct funds

When we look for expense ratio in short term it might not look major expense but small increase in expenses ratio will have drastic effect on your invested capital. We can observe that by below:

Invested Capital

₹ 1,00,000

CAGR

15%

Regular plan Expenses Ratio

2.50%

Direct Plan Expense ratio

1.75%

Years

Regular value ₹

HPR%

Direct Value

HPR %

Difference

1

1,12,125

12

1,12,988

13

863

3

1,40,964

40

1,44,242

44

3,278

15

5,56,592

456

6,24,390

524

67,798

40

97,29,673

9629

1,32,19,529

13120

34,89,856

This illustration clearly demonstrates benefits of investing in direct plan rather than investing through distributors.

The statistics given below show the growth in investments through a direct plan.

Some example of Mutual funds Regular vs Direct plan –

These are few points that should be kept in mind before investing in mutual funds. Other relevant aspects highlighted in bold over the article along with information on types of mutual funds and their costs will be explained in the following articles.

Author Harsh Shah Team Member- Alternative Investment (M.Sc. Finance, NMIMS – Mumbai. Batch 2019-21)

The other day I received an SMS saying invest Rs. 5,000 every month till the age of 60 and get Rs. 30,00,000 lump sum and Rs. 25,000 every month post the age of 60. I am sure every one of us is bombarded with these kinds of messages every other day. There are several online calculators available to check how much you should invest now to get the desired amount at the age of retirement. But what if you don’t have that much amount to invest in? Also, do you know much return your current investment should earn to generate a corpus for your retirement? To be honest, I didn’t know so I guess we are sailing on the same boat.

So without wasting any time, let’s see how can you use our tool to know the Return on Investment (RoI) required on your current investment to generate a corpus for your retirement in just 3 steps. Download the sheet from here.

What are the objectives of this sheet?

The whole purpose to build this sheet is to tell you how much return your investment should earn so that you can generate the desired corpus for your retirement.

What are the questions will be answered by this sheet?

You will know how much RoI needs to be earned on your investment. You will also know the amount you require to retire with. It also calculates your per annum post-retirement expense.

For illustration purposes let us assume there’s someone called Mr. X. He is 25 years old. He wants to retire at the age of 60 and expects to live till the age of 85. His current salary is Rs. 95,000 per month.

Follow the

below steps to get your questions answered:

Step 1: Enter your personal details

Here, you

are required to enter your current age, age at which you want to retire and age

till which you are expected to be alive. Please

note, this sheet is designed for a person who is more than or equal to 25 years

old and expected to live till the age of 99.

Step 2: Enter your per month income and expense

In this step, you are required to enter your current per month salary. Expected every year increment in salary and bifurcation of a monthly expense. Please note: It is required that saving as a percentage of income to be more than or equal to 15% (Otherwise person either has to increase his salary or reduce his expense)

Step 3: The easiest step among all

One only has

to press submit the inputs enter by one.

The output of the sheet:

The Output

indicates how much person has invested till retirement and what RoI he should

target on his investment. If a person manages to get the RoI calculated by this

sheet, he can achieve his corpus by the time he retires. ( Basically, in this

case, Mr. X has invested Rs. 1.44 Cr. till 60 years and he has managed to get

RoI of 12.44% on his investment. So at the age of 60, he has generated a corpus

of Rs. 20.26 Cr. which will take care of his post-retirement expense.)

This graph indicates how generated corpus will be depleted over a period of time

This graph indicates the proportion you have invested and corpus generated by your investment with RoI calculated by the sheet

So those who are interested to know the math behind this, here we go!

Following

are the few assumptions made by me while preparing the sheet. Please refer the

same.

Let’s look at the Expense tab:

Expense

sheet indicates how your expense will grow over a period of time. To be on the

safer side I have considered 13 months as annum. I have also considered growth

rates of each expense heads will remain the same for a decade and will be

revised by 0.5% compounded annually (Can be edited as per your

requirement).

Salary and investment tab:

We know our

annual salary and annual expense. Annual saving is just a difference between

income and expense. I have kept 5% (editable input) aside as an emergency fund

which will be kept aside in savings account. Available per month funds to

invest is remaining funds in hand after the emergency fund is kept aside. Now,

Corpus generated is a sum of funds in hand and money parked in a savings

account. (Note: Funds in hand should fetch min. RoI as shown in the output box)

Corpus tab:

Corpus sheet

indicates post-retirement annual expense and how that corpus will be depleted

over a period of time to cover your expense. Here I have considered the

generated corpus will fetch 3% post-tax return on the corpus (Pre TAX savings

return is 4% -editable input).

Hope this article has helped you to understand your target RoI on current investment and required corpus to retire on desire age. Let me know topics you would like me to cover in next post in the comment section below.

It’s an age long debate as to which is considered to be better in terms of an Investment Avenue. While both happen to be reasonably good options, due to its inherent nature, a lot of times ETF’s and Mutual Funds can be used interchangeably. In reality however, it is important that these asset classes have their own nuances that make them inherently different. In our innaugral post at Finvert, we will break down how these two securities are different and what are the things an investor should consider whilst investing in any one of the two.

What are ETF’s (Exchange Traded Funds)?

As the name suggests, an ETF tracks a particular index and allows the investor to buy the entire index as it were a stock. An ETF is therefore listed on an exchange and requires a Demat account for buying and selling of the fund. This lead to the name, ‘Exchange traded fund’. Due to this, ETF returns do not significantly vary from the overall market performance. ETF’s makes an ideal investment opportunity for Investors looking to beat inflation and expecting standard market performance based on historical data. The main attraction of an ETF is an overall lower turnover and expense ratio. These factors have contributed to high popularity enjoyed by ETF’s in the U.S. but not so much in India. The size of ETF’s in India seems poultry when compared to the AUM (Asset Under Management) of the countless mutual funds on offer in the market right now.

What are Mutual Funds?

Mutual Funds are a collection of a pool of money from different investors creating a fund which is actively/passively managed by a fund manager whose primary aim is to beat the returns offered by the stock market. Mutual funds can invest in various securities including stocks, commodities or bonds. A fund manager routinely changes the asset composition multiple times in a year so as to get the desired returns. This means higher turnover and hence, high expense ratio. Price is calculated daily at the end of the day based on fund performance. The entire money invested is then converted into units and sold for money.

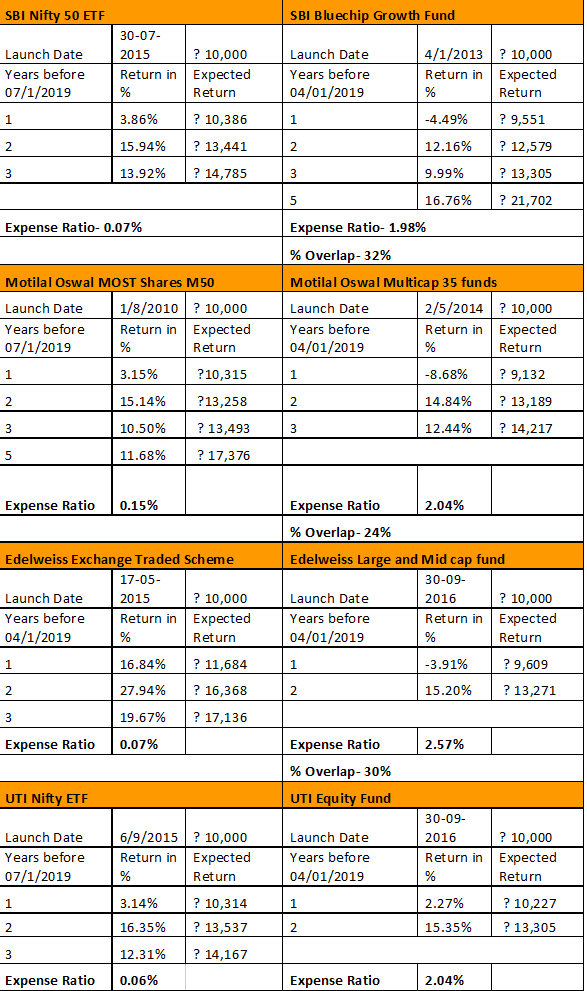

Mutual funds have burgeoned in terms of popularity in India due to the fantastic returns offered by the same in the past few years. Here we have taken some of the high performing ETF’s and Mutual funds of well-known fund houses and analysed the fund on various factors which include its returns, the expense ratio, percentage of stocks that are overlapping, etc. For a more like-to-like comparison, an ETF and a large-cap mutual fund is selected from the same fund house. Likewise, five ETF’s and five mutual funds are selected for the purpose. The returns calculated are rolling returns and also states the expected amount return when 10,000 are invested in the said scheme.

Comparing a year’s return between

securities is too short a term to perform a comparison. A three or a five year

term is enough time to perform a comparison. Looking at the table, the most

important distinction between the two is expense ratio. Where mutual funds

generally charge anywhere around 1.75-2.5%, ETF’s get away with 0.05-0.15% as commission

charged due to its passive nature. Add to that the turnover ratio (number of

times stocks are bought and sold) of a mutual fund is high which also increases

the overall expenses of the mutual fund. Things become interesting when tax

comes to picture. Essentially, mutual funds are taxed yearly whereas capital

gain tax on ETF’s can only be taxed when they are sold.

Overlapping of stocks in the security portfolio is another interesting thing between an ETF and a mutual fund. For eg., ICICI Prudential Nifty ETF and ICICI Bluechip fund direct growth have 74% of the stocks in their kitty that are similar. So ideally the returns for the same should match to a certain extent and that is very much the case for a 3 year period. But the mutual fund at 15.77% still manages to outperform ETF at 12.91% in the long term five year period. Another

The most important purpose of any investment is the returns generated and this is where mutual funds outperform ETF’s most of the time. The return is high but when factors such as expense ratio, stock turnover and tax come to picture, both the securities seem to offer similar returns. In some cases, ETF’s actually outperform mutual funds which question the whole idea of alpha generation in mutual funds in the first place.

While all this may look like a good picture for ETF’s, the reality is that ETF’s fail miserably in one important factor for any investor viz. which is liquidity. While mutual funds have grown to be very popular in India, ETF’s are very new and minuscule in comparison. So whilst the buying aspect may not be a problem, selling an ETF might be. So the investor needs to be cautious of this fact beforehand. But this being the stock market, no word is absolute and so both the options are to be considered by the investor while looking for an asset class to invest in.

This is not to be considered financial advice in any manner. Do your research before investing in any of the mentioned assets. Our work is limited to educating our readers regarding the same.